Episode Transcript

[00:00:01] Speaker A: Welcome back for another episode of Unscripted Small Business. Today's guest is Doug Johnson, a licensed CPA based out of the Golden State of California. Doug started his career at Ernest Young, one of the largest accounting firms globally. During his time in corporate, he worked with Fortune 500 clients before transitioning to GoodRx, a multi billion dollar company based in Santa Monica. But despite his success in the corporate world, Doug felt called to make a more personal impact, which led him to start his own accounting firm where he sees himself as a partner, focusing on helping small businesses and professionals navigate their tax and accounting needs. In this episode, Doug opens up about the challenges and rewards of entrepreneurship, the importance of accessibility in accounting, and offers insightful tips on business structures, tax deductions, and when it's time to hire an accountant. Whether you're a business owner or are just looking to optimize your finances, this episode is packed with valuable advice. Let's get started.

[00:01:08] Speaker B: With Tax season upon us, I am so excited to have our guest in the studio with us today. Doug Johnson is a CPA joining us from California. Doug, it's so great to have you in the studio.

[00:01:18] Speaker C: Thanks, Abby. Appreciate it. Thanks for having me on.

[00:01:21] Speaker B: So, just to get started, tell us a little bit about your background and how you kind of got started with accounting.

[00:01:27] Speaker C: Yeah, a hundred percent. So to take it all the way back, I suppose I was in college, I went to USC and I was majoring in business at the time. Didn't really feel like I was learning a whole lot in just general business classes. I'm not sure what I expected, but just didn't really feel like I was getting much out of it. And then took my first accounting class and felt just the total opposite way. Felt like I had learned an applicable skill, almost like a, like a trade of sorts. So that was my freshman year in college. Knew from that point on that I wanted to just pursue that as a career and so changed my major to accounting and went from there. So I'm not sure, you know, if you or anyone else are aware, but the, the pipeline from college into the big accounting firms is, is pretty robust, especially at a school like usc. So just had a job pretty much lined up since my sophomore year, which was great, since most college kids are petrified that they're not going to get hired.

So spent about a year working at Ernst and Young, which is just one of the big four accounting firms, and did what's called technical accounting advisory. So basically it's just writing and researching about accounting and writing like 20 to 25 page papers on it. So I actually. It sounds terrible. I did enjoy that actually. I really enjoyed the research. Research aspect.

Did like some light tax and audit work there as well. But overall knew pretty much immediately that I didn't want to be in that kind of corporate environment. And so after about a year moved over to a company called Goodrx which was at that time a little bit more startupy. It was about 300 ish employees but still had startup feel. So did more just general accounting work there. Some, a little bit of again, light tax and kind of similar feeling. I mean, I enjoyed it there a little bit more than working at a big accounting firm, but knew, you know, I didn't want to be in corporate.

That was my eventual goal. Just don't be in corporate, work for yourself. And so just started working with some clients here and there doing, you know, bookkeeping, projects, tax, that sort of thing. And then in conjunction with that also built up a little real estate investment business as well. So that's kind of unrelated, but that real estate investment business actually gave me the cash flow to just decide I'm going to go out on my own earlier last year and so have just been working those two businesses in tandem. And so, you know, when you, when you have real estate, you're investing in it once you buy it. In a lot of cases, there's not a ton left to do before you sell it. So basically I use the time in between deals to grow my accounting firm.

[00:04:23] Speaker B: Well, that's awesome. Well, Doug, congratulations on owning your own firm and also with all of the real estate development as well. That's incredible.

Tell us a little bit about how your corporate background kind of got you prepared for working with small businesses.

[00:04:37] Speaker C: Yeah, a hundred percent. I think the biggest thing is just a lot of times small businesses are not used to processes and systems that are expected at a bigger business. So, you know, I mentioned I worked in kind of a startupy environment. A lot of what we did there was just things were changing so fast that we needed to build a new process pretty much every week. There was always something new happening that was going to scale up in the future that we needed to figure out how to account for. And so that was, that was a great experience because you're, you're building a scalable system pretty much every week is what we were doing at that point. And so that eventually tailed down. But those skills are the exact sort of skills that you need to work with small businesses. Their business is not always going to be the same. A lot of Them are pivoting. And so I think what I have found is that a lot of people in small business, they're great at the trade or the business that they do. You know, like they, they're a great marketer, they're a great plumber, but they're not necessarily so good at scaling the back end side of their business. And so that's, that's really where I come in and help people.

[00:05:49] Speaker B: Awesome. I actually have some more questions about scalability as we kind of progress into our conversation, so I'm excited to touch into that. But tell us a little bit more about starting your own firm. I mean, that's a really big move to make. What's been the most challenging aspect of making that transition?

[00:06:06] Speaker C: Good question.

I think, I think at the beginning, the hardest thing was uncertainty. I remember basically the day after I quit my corporate job, actually it might have been like that night.

It was a great job. I worked with people I really liked working with, got paid really well, especially for my experience.

And I was stoked initially because it felt like a dream to be able to go out on my own. But then like, existential dread just hit me and I'm just like, what did I do with my life that was, was this the dumbest thing I've ever done?

So I think in the beginning, especially as I was building up a client base, it was, yeah, just the uncertainty was really hard because I was constantly thinking, okay, what if this doesn't work Now I have to go back to corporate life, which I wasn't a huge fan of. And I had a great job. Like as far as accounting jobs in the corporate world went, mine was incredible. So just having to, I think having to face the fact that I would probably have to take a downgrade if I went back, just fueled me to just make something happen. I had to.

[00:07:19] Speaker B: Yeah. What advice would you give entrepreneurs who are kind of in that position where they, they're feeling that fear, but they, they gotta, you know, push forward.

[00:07:30] Speaker C: I, I think it's, it's natural. Like you're, you're always gonna feel that, I think at every stage, you know, like if you try to do something new, if you pivot your business, like, I think one thing I've learned both from the accounting business, but especially from, from the real estate business I have is like a great opportunity is almost never going to exist forever. You need to jump on it while it's there, and then inevitably you're going to have to adapt in some way. And so I think like there's there's always going to be uncertainty. You need to just learn to live with that power through it. And like I kind of alluded to earlier, like, that that needs to fuel you to just make it, because I think it can either paralyze you or just make you determined to succeed. And I definitely felt a little bit of both.

[00:08:23] Speaker B: Well, and I think what's cool about what you're doing, too, is that you mentioned that you don't just see yourself as an accountant, you actually see yourself as a partner with your clients for their ultimate success. Explain to us what that looks like in practice.

[00:08:36] Speaker C: Yeah, so glad you touched on that. Actually, I think that was when I was thinking about the kind of practice that I wanted to build. I kind of saw a gap in the market there, I think. Um, yeah, I spend a lot of time online. Um, I see a lot of people complaining about their accountants. And, like, the two biggest complaints that I saw consistently, number one was, I can't get ahold of this person. Um, and so that. That is still like my number one guiding principle beyond just doing good work is just, I need to be accessible to the people that are paying me. And then two was. And it's kind of tied into that same idea is my accountant is just doing my taxes at the end of the year, and I'm getting no guidance throughout the year.

And I totally get that. And that's. That's where I find I can add the most value. Like, I worked for a pretty large company, managed a ton of the expenses there, and just got an insight into how large businesses work and just how, you know, decisions you make can change the financial performance of the business. So I think that's actually where I'm able to provide the most value, is just saying, hey, here's what your financial performance looks like. Now. Here are the levers that we might have to drive more revenue. Here's where, you know, maybe costs are a little bloated, that sort of thing. I think one good example is advertising. Like, a lot of small businesses, they'll kind of dump money into advertising. They don't necessarily know how much they're spending. Maybe they are spending on five different platforms. They don't really have the time to pull it all together. And then, like, they don't think about, okay, if I increase my advertising spend, is my revenue increasing? So that's. That's one area that's just an easy win. Always, every time I work with somebody new, if their advertising spend is high, we just laser in on that and make sure we're understanding what goes into that and is it actually driving results? Same thing with like payroll, just other things like that.

[00:10:37] Speaker B: I love that you mentioned that you're accessible all year round because like you said, a lot of business owners are really just thinking about taxes towards the end of the year. And now that it's kind of that time, that's where a lot of the focus is going.

But what advice would you give to entrepreneurs who maybe they, they don't think that they need to work with an accountant right away starting a small business. When should they incorporate an accountant into their mix?

[00:11:01] Speaker C: I think it's kind of a cost benefit question that you're asking there because you know, on one hand an accountant is, is not cheap. Like I'll be, I'll be, I tell everyone this like I'm, I'm not going to be the cheapest tax pro out there. I'm totally okay with that. And that's because I'm going to provide you with better service and more accessibility than pretty much anyone else. And so, you know, if you're just starting a business and you have 10,000 in revenue, probably not the best choice to go out and spend a good chunk of that on an accountant, I think.

And part of it depends on the state that you're in. But maybe at about like a hundred K in net profit is kind of where it starts to make sense to incorporate some tax planning because there's easy wins that everyone can do. Stuff like, you know, make sure you're contributing to your retirement accounts, that sort of thing. You don't need a, you shouldn't need a tax pro to advise you on that. When you get to about 100k in net profit, that's where things like, you know, should you become an S corp? That is a question that you might want to have somebody analyze for you. This is more of a technical tax topic, but stuff like electing into pass through entity tax, that's again something that's going to come into play like the 100k plus level.

And those are things that not everyone is necessarily equipped to do on their own. Before that point. I think, you know, it can make sense if, if your revenue is, you know, 200k plus and your margins aren't, aren't at that 100k net profit. But I think in those earlier days you're probably better off spending your money on advertising or just, you know, figuring out how to operate your business.

[00:12:46] Speaker B: I really love the honesty and I really appreciate that.

That kind of leads me into my next question. Talking about different business structures. Let's say a small business owner decides that they want to be, you know, a sole proprietor and then they're like, I need to move into something else. Do you ever see that the, the change or transition into business structures affects the tax and the accounting side of things?

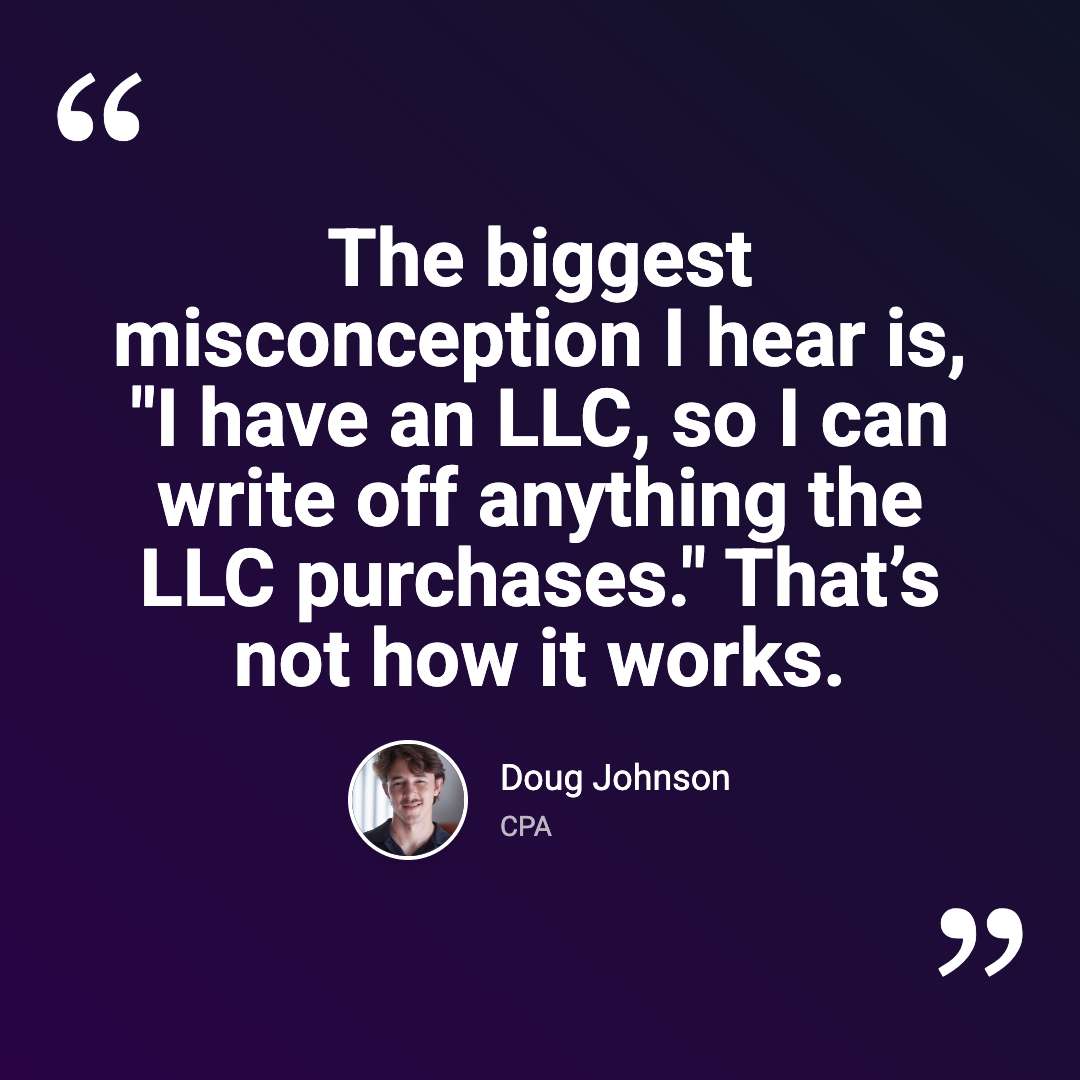

[00:13:12] Speaker C: Yeah, oh absolutely. I think, you know, most of the time people are going to start out. A lot of times people won't have an LLC that's totally fine, that, that has no tax purposes, which is a common misconception and something I have to explain to clients all the time. They're like, I need an LLC to deduct all these expenses. And I tell them, no, you don't.

You know, I live in California so it's a, it's a common mistake. People say, oh, I have to get an LLC for my business, that makes 20K. Okay, well now you're paying California $800 essentially for nothing. So that's a common misconception. But I think, you know, around that 100k net profit range, that's where something like an S Corp can make sense. And that's essentially, it's a strategy that allows you to shield some of your business's net profit from self employment tax. But I think those, the disadvantage of a change like that, ignoring the tax side of things because there are, there's pros and cons with every tax strategy. And that's certainly true for you know, an S election as well is it just makes things a little bit more complex.

For instance, you know, any, pretty much any time I get an S corp return from somebody who has self prepared it, it is not correct. And so that is going to cost you additional fees in terms of just probably not amending it. But getting it correct in the current year is going to be a little bit harder for whoever your CPA is. And then, you know, let's say it's incorrect in 2023, you want to correct it in 2024. You know, even though you might not have to go back and amend, there is a slight risk in leaving it incorrect that I always make people aware of. So I think, yeah, whenever you change your business structure from anything besides just schedule C, single member llc, sole proprietorship type deal, that that's where people kind of start to get in trouble on the tax return side of things in.

[00:15:10] Speaker B: Terms of making those changes. Are there certain legalities that you run across when people do it wrong or is it mostly just kind of fine penalties?

[00:15:23] Speaker C: So I mean a lot of it is just, I think it's important to understand that. So for instance, like an S corp, a partnership, those, those are called pass through entities. Those entities are audited at a super low rate. It's like something like half a percent.

So the probability of you getting dinged for something is low. But you know, let's say you did something incorrectly depending on the nature of your error. Sometimes it's just a presentation issue that can cause headaches down the line if you're to sell your business, something like that.

But you know, sometimes one, one common mistake is people will elect into an S corp, they won't run payroll for themselves and then they're stuck dealing with that after year end. There's workarounds for that that are going to get you essentially to the same net tax effect.

But there have been cases in tax court where, you know, people implement these workarounds. Sometimes they do it for years and years and then the IRS will come after them and say, hey, okay, you paid the self employment tax, et cetera, but you know, you didn't make the filings that you were supposed to with regards to payroll taxes. Now we're going to come after you for failure to file stuff like that. So it's not again, it's not super common unless you're I guess just doing something that's going to trigger red flags on the IRS computers. But it is a risk and over a long enough period of time, like you don't want to increase your risk level.

One other thing just to add is beyond, beyond penalties and fines, you know, if those are assessed, like dealing with a tax agency is a headache and like the cost of your time should not be excluded from that calculation. I would say absolutely.

[00:17:13] Speaker B: Let's talk about some of the misconceptions that businesses might have when it comes to tax deductions and write offs. Tell us a little bit more about where small businesses might be able to find write offs and some of those misconceptions that people might have.

[00:17:29] Speaker C: Yeah, so I think it's, it's, yeah, it's, it's, it's a good question. I think a lot of the time the biggest misconception I hear people discuss is I have an llc. I'm going to write off anything that this LLC purchases is now a business expense. That is it. It doesn't make any sense, but people still think that that is the case. And so people will, you know, buy something that is clearly personal use and then they will attempt to deduct it as a business expense. That does not work. I think one Great example of that is vehicles. People will, you know, buy a $30,000 truck and say, well, I use this for business. It's a business expense. Well, if you use it 10% of the time for business, that's not a business expense. You can, you know, you can get reimbursed for mileage, etc. There's, there's still a business component of that that is an expense, but it's. You can't just deduct the whole 30k. And to that point, that is one of the biggest areas of audit is vehicles. For that exact reason. I think the other thing that is commonly misconstrued is when people, they'll say, oh, okay, I have a high tax bill. I need to buy something to offset this. I need more expenses.

I don't really follow that train of thought because generally, if you have a high tax bill, that means that you made a lot of money. So that that's a good thing. Taxes are an inevitability for the most part, you know, especially at the small business level, where you're not operating extremely complex structures, things like that. And the other thing is to, you know, let's say that you buy a truck for 30k and it is actually a business expense. That doesn't mean you're reducing your tax bill by 30k. You are reducing your tax bill by 30k times whatever percent your tax rate is. So if your federal tax rate is, let's say you're in the 32% bracket, you're getting a tax savings of like $9,600, which is still great, but it's not. It's not to the extent people think. So I think one thing I always try and tell people is, you know, don't. Don't just buy something to reduce your tax bill. If you need something for your business and you were planning on buying it next year, but you need it and you have a tax liability you want to offset, okay, buy it this year. You still needed it for your business. But I think when people start, when they start just incurring expenses for the sake of reducing their taxes, that's, you know, they're stepping over a dollar to pick up a dime.

So hopefully that mostly answered the question as, as far as, you know, finding expenses. I think for the most part, I tell my clients, just come up with anything that you think could be deductible. You know, I can help you make that determination as to whether or not it is.

And the easiest thing I think people can do if they're not super organized from the get go is just get a business bank account set up because you know, aside from, you know, legal protections, when you think about collecting your expenses at year end, do you want to have to go through your personal credit card account, your personal bank statement? No. You've got a million other things in there. The chances of you missing something are so much higher than if you just have a business bank account right away. You know, everything is right there. So it's, it's still work. You're going to have to classify it, but your chance of missing something is near zero when you do that.

[00:21:03] Speaker B: That's really, really good advice. And I love, you know, everything that you said about deductions too because I think that that like you said, that is a really big misconception is, and as somebody that you know, does self employment stuff, I think about the deductions that I can have and things like that. So it is important to, to know where you shouldn't be making those deductions.

So if, if not for deductions, tell us some other key strategies that businesses could have to optimize taxes throughout the year so they're not scrambling when it comes tax season.

[00:21:33] Speaker C: Yeah. So there's so many ways you can go. I think one, one thing actually that I'm kind of dealing with some clients right now is what I like to call tax sticker shock. You know, especially this is for somebody who, let's say their business, they start a business early in the year and it did really well, or maybe their existing business, you know, profit went through the roof in a given year.

They are not used to having to pay taxes on this amount of income. Maybe they didn't make estimated tax payments. And so when you get to the end of the year, not only are you going to have underpayment penalties, maybe that it depends on what your prior year liability was and what other income you have. But you're just going to be faced with this huge bill and it's, it's shocking.

And I remember I, it happens to me sometimes. I remember when I was early in my real estate investment career, I had a, I had a great year and I got to the end of the year and filed my taxes and I was like, whoa. And it's, it sucks. And I think the biggest thing that you can do to reduce that is just make sure you're making your estimated tax payments throughout the year. Not only are you avoiding underpayment penalties by doing that, but equally importantly I think is you're just making it Easier to face the tax bill when you pay it throughout the year. And you're not just. Yeah, because it can, it can be a shock. So I always try and get clients to pay as much of their estimated tax payment or estimated tax liability as they can.

They're, you know, there's not always reasons to do that. Let's say, you know, you don't have to make a certain tax payment amount based on your prior year liability. You know you're going to owe at the end of the year. What I'll tell some people is okay, hey, we know we're going to owe this much at the end of the year. Put that money in a high yield savings account right now. That way you're making money. No sense in giving it to the government right now. But there are some clients that I know if I tell them that they're going to get a year later and they're going to be pissed. And it's like, okay, for you, I'm just going to tell you to pay throughout the year.

So I think that's an easy way. Another great way for small business owners to save and this is, this is better for businesses with higher cash flow is small businesses, small business owners, they are able to put away a lot more into retirement accounts than W2 employees. So you know, in 2024 W2 folks could put away 23,000 unless you're over a certain age and it's 30,500. But we'll just go with the lower limit of 23K. If you're a small business owner, that limit bumps up to 69,000. Now that's, it's based on a variety of factors including your net self employment income. But you know, for, for those folks who are, you know, who own businesses profiting 300,000 plus a year, that is such a great way to just set yourself up for the future and also defer taxes now by maxing those increased limits. So that's a great way. Obviously S Corp. If it makes sense. It doesn't always, you know, some states tax s corps, New Jersey is a pretty big offender. New York is, it's tough to make the math make sense.

So that's a state specific question and that's often why I'll tell people don't make this decision without having somebody who does this for a living help you out. Because if you're in New Jersey a lot of the times you'll pay more in taxes by having an S corp versus less. And so a lot of people don't realize that they go through all the headache of an S corp and then they're set having to unwind it all. So that's, that can be a great strategy, but it's, it's, it's not DIY for the most part, I will say. And then the other big one that I've been trying to push for people is what's called a pass through entity tax election. And so essentially that is where the business will pay state taxes on behalf of the owner. And so what that'll help do is it'll circumvent the state and local tax cap on your itemized deductions. So when you file your year end taxes, if you itemize deductions, you're only able to deduct 10,000 in state and local taxes. So obviously for people who live in California, New York, high tax states like that, you're kind of getting hosed because your tax bill is going to be a lot more than that in most cases. So that pastor entity tax election is a great way to get around it. I will caveat by saying that there's a lot of uncertainty about what the tax code is going to look like beyond 2025, because that, so that salt cap, that, that local tax cap and that pass through entity tax election, those are set to sunset after 2025. But with a new administration, you know, it's been signaled that a new tax bill is a priority. So everyone's kind of in wait and see mode. So a lot of the things that I'll tell people are great strategies for 2025 might not exist in 2026. So we're, we're kind of in a holding pattern on a lot of items.

[00:26:43] Speaker B: Yeah, I want to touch on going back to deductions and making sure that businesses are tracking things appropriately, even just for your sake at the end of the year. I know you said having your own business bank account is really important, but what other ways can people track these expenses appropriately? Do you recommend keeping receipts? How can you itemize those items for deductions?

[00:27:08] Speaker C: Yeah, so for, for people who are, I guess, a little more bookkeeping savvy, I will say, you know, use a software like QuickBooks or Xero or pay somebody to do it for you. One arrangement that I have with some clients that has worked really well is these people will keep their books throughout the year and then I will hop in, you know, either on a quarterly or semiannual basis to just go in review, make sure that everything's being recorded correctly, and then we're not going to have to unwind something at the end of the year. So, you know, if you're bookkeeping savvy, that that is a great way to go about it. If you're not, a lot of times I'll just tell people, if you're at a certain scale, just hire somebody. Because otherwise, whoever your, your CPA is at the end of the year is going to be doing that for you. And then they're probably going to charge you more and they're going to charge you at a CPA rate, not at a bookkeeper rate.

So that would be my advice there.

As far as keeping receipts, the IRS does require receipts for everything over $75, all charges. So I think it's best practice to, to keep everything over 75.

In reality, it is a massive headache. And so I understand why people don't do it. But I do think even if it's just in a folder or something, it doesn't necessarily all have to be organized. Just, just do keep it because then you'll need to, if you are ever audited, you will need to substantiate it. And so again, audit is not super likely. But if you have all of your receipts organized, you have everything, and the IRS revenue agent comes and says, hey, I want to see documentation for this, this, and this. If you can just go provide that quickly and easily, you are going to be in and out of there. If you have to spend hours digging up something that you forgot that you even did, that, that is not a good time.

[00:29:04] Speaker B: What happens if you don't have a receipt but you have the bank statement with the purchase on it? Would that count in an audit or do they not accept it?

[00:29:13] Speaker C: So I would actually have to go back and double check on that. But I believe that that could be disallowed. I think probably depends on the agent that you got.

Some people are stakeholders.

[00:29:29] Speaker B: Keep your receipts. Everybody keep your receipts.

[00:29:33] Speaker C: Yeah, it's, it depends on the nature of your business. But like, if you're an online business, it's easy to do. Like you're going to get an email receipt. Every, every chance you get to get an email receipt, do that. That's going to be, that's easy. And then one thing, one thing I'm really pushing for, folks, is if you have any sort of mileage, use a mileage log.

That, that is one area that is historically audited because it's such an easy win for the irs. You know, if it's material enough, like if you have 600 miles, like probably not going to be a ton of scrutiny there because that's not going to be, that's not going to be a big win. But if you have a business that requires you to drive a ton, you're claiming a huge amount of mileage and you don't have any mileage log to substantiate it, that can get disallowed and that's a pretty easy win for the irs, that is.

[00:30:26] Speaker B: As a business owner, how do you recommend people approach their personal taxes especially if they're taking profits or income from their business?

[00:30:36] Speaker C: I think it's important to understand that everything is integrated. And so your question about taking profit from your business, how that is going to impact your tax situation is entirely dependent on the tax structure of your business. So you know, if you have an S corp, you need to make sure that you're paying yourself a salary before taking distributions.

So that, that's, that's kind of a more nuanced question. I do think it is important to understand that in pretty much every business structure besides a C corporation, which is not a good structure for a small business to have, you're going to be taxed on net profit. So it doesn't matter how much you pull out of the business, you're going to be taxed on the net earnings of the business. And that, that's something I see trip people up sometimes. They'll say oh well, I only took 5,000 out of the business bank account, that's irrelevant. The business made X amount and so you were going to be taxed on those, on those earnings.

[00:31:34] Speaker B: For small businesses growing rapidly, what are the key tax considerations when scaling especially if a company is trying build business across a different state?

[00:31:45] Speaker C: I think that the key tax consideration when scaling is number one, make sure your books are in order because that's obviously your books feed into the year end return. So if that's not accurate, your, your tax return is not going to be accurate. And, and that's, that's when you're scaling. You also need to just have good books to get an understanding of how your business is working. Like it's going to be really hard to scale effectively if you don't understand your financials. It's not impossible but you're, you're shooting yourself in the foot by, by not understanding your financials. And then second, I would say especially if you're expanding across states, make sure that you have a competent tax advisor to help you understand the tax implications of that and make sure that this person understands, okay, I am now I have income in this State, I need to be making estimated tax payments to this state, things like that. Most CPA firms are not going to help with stuff like sales tax because it's honestly, it's a big liability and it's something most firms don't want to touch, myself included. But if that is something that is applicable to your business. So for instance, a lot of E commerce businesses will have considerations on that front. There are firms out there, like bigger companies, one of which is Avalara, that can, that can assist you with that. I will say that I have not heard great things about Avalara, but that is the one that I know of. But yeah, I mean, sales tax is a tough one because like I said, most terms aren't going to touch it. There's too much to know and it's just, it's too much risk for what you get out of it as a firm. So you gotta be fully honest there.

[00:33:28] Speaker B: Well, we appreciate your honesty, Doug, and I can just tell that you have just a lot of wisdom about this.

As somebody that's based in California, can people across the nation work with you, or do you only work with businesses that are based in California?

[00:33:43] Speaker C: So that's actually another. You kind of touched on another common misconception. CPAs for the most part, can, can work. They need to have a CPA license in the state where they reside and where they actively practice. So for me, that's California. But I can prepare tax returns, advise on tax matters in any state besides Hawaii. And so that's going to be the case for most CPAs. You know, somebody is a CPA in Ohio, again, they're going to be able to help somebody who's in California. I think where you might want to go with somebody local is, you know, let's say if you're state happens to have particularly onerous local tax rules. So I think one, one good example of that is, you know, Portland, Oregon, Multnomah county specifically has, you know, they have some small taxes that most local jurisdictions don't have. So, you know, I happen to have an understanding of that because I have a few clients out there. But there, there are going to be jurisdictions like that that just have little taxes that other Preparers and other CPAs might not be aware of. So if you live somewhere like that, maybe go with somebody local.

But ultimately, I think the most important thing is just finding somebody who suits your needs, is able to provide you with the expertise that you need, who's responsive and that you like working with. So for me, I, I have clients all over the country. Like I said, I will work with anyone besides folks with Hawaii tax implications. And yeah, I. I welcome the opportunity to learn more about other jurisdictions, as I think most CPAs do.

[00:35:21] Speaker B: Very cool. How many people are in your firm currently?

[00:35:24] Speaker C: So it is just me. I will probably be hiring late 2025, early 2026. We'll see.

[00:35:34] Speaker B: Very cool. And are you accepting new clients?

[00:35:37] Speaker C: I am, yes. So more focused on small businesses, but I do accept individual tax clients as well.

[00:35:46] Speaker B: Wonderful. And where can we learn more about your firm and get in touch with you?

[00:35:51] Speaker C: Great question. You can go to Doug johnsoncpa.com so it's hopefully it's a pretty simple name to spell and then you're also welcome to just look me up on LinkedIn. You can either find my firm or me there and that's probably the best way to get in touch with me. People can also, if you'd like, you can reach out directly@doug ug johnsoncpa.com but most people just prefer to go through the website.

[00:36:18] Speaker B: Wonderful. And I will link your website in the show notes. Doug, I have one more question for you, and this is a question that I ask all of my guests at the end of the show. And it's kind of one of those mad lib, fill in the blank questions. So the question is you have to blank to blame.

[00:36:37] Speaker C: That's a good question.

I there are a lot of great answers to that, but I think the one that would be most applicable to this podcast would be you have to take risks to build the life you want.

I think that is applicable to all business owners. You are almost never going to have a situation where, you know, starting a business is is going to be without risk. So I think that's it's not only applicable to business, but just to other parts of life as well. You know, like if you want to travel the world, you're going to have to take the risk of leaving behind everybody you know at home, stuff like that. So I think that would be my answer.

[00:37:22] Speaker B: I absolutely love that. Doug, it has been an absolute pleasure having you on the show. Thank you so much for your time. And I'm really looking forward to just having our listeners hear these insights. So thank you so much.

[00:37:32] Speaker C: Thank you, Abby. I really appreciate you having me on.

[00:37:37] Speaker A: Thanks for tuning in to today's episode with Doug Johnson. I hope you found his insights on accounting, entrepreneurship, and tax strategies as valuable as I did. If you're a business owner or professional looking for more personalized guidance, Doug's approach could be just what you need. So be sure to check out his website and take action on some of the strategies he shared today. And if you enjoyed this conversation, don't forget to subscribe, rate and leave a review. And as always, feel free to share this episode with anyone that you think could benefit. As Doug said, you have to take risks to build the life you want. We'll see you next time.